For years, most retailers have treated payments as a fixed cost you budget for and try not to think about too much.

Zyntrix was built on the conviction that this is the wrong way to think about payments.

Zyntrix is a UK-based fintech that combines open banking payments, built-in loyalty and digital ID verification into a single platform for retail businesses. It has just been named one of the 50 most innovative retail technology companies in the UK, ranking fourth in BusinessCloud’s RetailTech 50 for 2026.

The ranking was decided by a combination of reader votes and an expert judging panel that included Scott Thompson of the Retail Technology Innovation Hub, Catherine Erdly of The Resilient Retail Club, and Joe Stevenson of Alvarez & Marsal. It celebrates British businesses of all sizes creating original technology for eCommerce and bricks-and-mortar retail.

Zyntrix.io – open banking payments, loyalty and digital ID for retail

What is Zyntrix and what does it do?

Zyntrix is a payment-led growth platform built on open banking rails. It combines three things that most businesses buy separately and try to stitch together.

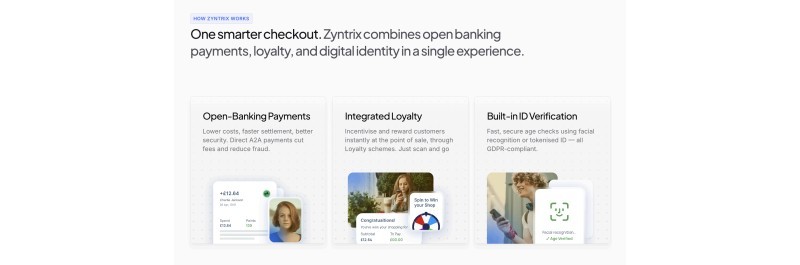

How Zyntrix.io works

When a customer pays via open banking, by scanning a QR code or using a pay-by-bank link, the transaction completes without a card network being involved. The fee saving is calculated in real time. A portion of that saving is automatically credited to the customer’s loyalty balance, under the retailer’s own brand. The platform is also capable of verifying customer ID – a serious benefit to businesses dealing in regulated, age restricted categories.

The merchant, meanwhile, receives full transaction data: who paid, when, how often, and what their relationship is worth over time.

Checkout is not the end of the customer journey. With Zyntrix, it is the trigger for the next one.

Why open banking payments matter for UK retailers right now

British retailers are navigating one of the more demanding trading environments in recent memory. Margin compression, rising business rates, the ongoing cost of acquiring and retaining customers, and loyalty programmes that typically require their own budget to run are all pressing in at once.

The retailers most actively seeking new technology right now are not browsing for nice-to-haves. They are looking for things that move the numbers.

Open banking payments, which route transactions directly between bank accounts without involving a card network, offer a genuine structural shift in how those numbers can look. Transaction fees on card payments typically sit between one and three percent. Removing the card network from the equation reduces that cost significantly.

The question for most retailers has been whether the customer experience at checkout is good enough to make the switch viable at scale. Zyntrix’s case for why the answer is increasingly yes is worth reading in full: Open banking in retail: a missed opportunity.

The person leading Zyntrix

Tom Hill, CEO of Zyntrix, brings over 20 years of retail and hospitality experience to the role, having held senior positions across brands including Sainsbury’s, KFC, SSP and Poundland. Most recently, as Director of Digital at Poundland, he led the launch of the retailer’s loyalty proposition and wider digital transformation.

He is not approaching retail payments as an outsider. He has sat on the other side of these conversations — where payment costs are a margin pressure to manage, loyalty requires ongoing investment, and operational teams are rightly cautious of anything that risks slowing checkout.

That experience shapes everything about how Zyntrix is built and sold: commercially grounded, operationally realistic, and designed to work within the constraints retailers actually face.

Tom Hill, CEO of Zyntrix, on the future of payments

Today, Tom is focused on positioning open banking as a genuine growth lever for retailers — not just a cost-saving mechanism. He was recently invited to contribute to a Bank of England and UK Finance workshop series on driving account-to-account payments at checkout, alongside leading retailers, banks and fintechs, and regularly shares perspectives on the future of payments, loyalty and customer data.

Follow Tom on LinkedIn where he regularly shares insights and news on open banking, loyalty and retail.

What makes Zyntrix different

The before and after of Zyntrix

Most payment technology optimises one part of the process. Processing is handled by one provider, loyalty by another, customer data by a third. The integrations between them are built and maintained at the merchant’s cost, data sits in silos, and reporting rarely joins up cleanly.

Zyntrix is designed to optimise the whole loop through a single integration. Payments, loyalty and identity verification, including built-in age verification at the point of sale using facial recognition or tokenised ID, all sit within one platform.

Once the integration is complete, it scales across locations without repeating the heavy lifting.

There is also a transparency argument. Where most payment providers profit from complexity and hidden fees, Zyntrix makes savings visible at the moment of payment. When a customer sees that a transaction has generated a loyalty reward, it creates a positive brand association that staff naturally mention and that operators discuss with peers in their networks.

This is how B2B products build organic momentum without relying on advertising spend to carry the message.

Zyntrix at Retail Technology Show 2026

Come find Zyntrix team at Retail Technology Show 2026 in London

The Zyntrix team will be at the Retail Technology Show at ExceL London on 22 and 23 April 2026.

If you are attending, it is worth finding their stand. The team will be on site recording interviews with retail leaders, covering open banking adoption, loyalty strategy and the shifting economics of retail payments. If you work in retail and have a perspective worth sharing, reaching out in advance is a good idea.

For retailers curious about whether open banking payments are a realistic option for their business, the Zyntrix team can model the numbers against your specific transaction volumes and current fee structure. The conversation tends to be more concrete than most technology demos.

Frequently asked questions about Zyntrix

What is Zyntrix?

Zyntrix is a UK-based fintech platform that combines open banking payments, a loyalty programme and digital ID verification into a single integration for retail businesses. It is designed to reduce payment processing fees, increase customer spend and give merchants full ownership of their transaction data.

How does Zyntrix reduce payment fees?

Zyntrix processes payments via open banking rails, routing transactions directly between bank accounts without involving a card network. This removes the 1 to 3 percent fee that card processors typically charge on each transaction, with the saving calculated and displayed in real time at the point of sale.

What types of businesses use Zyntrix?

Zyntrix is suited to scaling businesses with recurring revenue and frequent transactions, including gyms, dental practices, care homes, hospitality groups and multi-site retailers. The platform is particularly valuable where margin efficiency and customer retention are commercial priorities.

Is Zyntrix available to retailers across the UK?

Yes. Zyntrix is a UK-based fintech headquartered in London and works with businesses across the United Kingdom. The platform is built on UK open banking infrastructure and is designed to integrate with existing point-of-sale systems without rip-and-replace installation.

Find out more

Visit zyntrix.io to explore the platform or book a demo. To stay current on open banking, payments and loyalty thinking from someone who has worked inside retail at scale, follow Tom Hill on LinkedIn.